Prof. ST Hsieh

Director, US-China Energy Industry Forum

626-376-7460

February 5, 2022

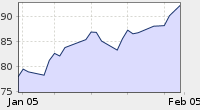

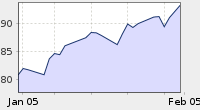

The following charts show that both WTI and Brent benchmark oil prices have been rising fast since last month. Further, the gap between Brent and WTI seems to be narrowing, the difference today is only US$0.96 while it should be around US$2.00. The narrowing price gap indicates that the market considers the geopolitics risk for the US is approaching that of Europe. The target price soon is above US$100/bbl.

Obviously, Russian and US war talks over Ukraine crisis is a major driving force. Even though a full-scale war in Europe will cause a severe global economy downturn, thus less energy demand. But a large-scale war will cause global energy production and transmission breakdowns. Global energy price will rise! The main drag on global crude oil price is the uncertainty: how long will this crisis last. Peace is always preferred over war!

Friday, February 4th, 2022

WTI Crude Oil | |||

$92.31 | ▲2.04 |

| 2.21% |

2022.02.05 end-of-day |

$93.27 | ▲2.16 |

| 2.32% |

2022.02.05 end-of-day |

There are other contributing factors.

- Weather related seasonal event: A massive winter storm sweeping across the US reached the Permian Basin, triggering fears of potential supply disruptions in the largest American shale play. It is a short-term and localized issue so the impacts should be over within weeks at most.

- Accidents: Explosions in Nigeria and landslides in Ecuador affecting crude productions. Combined crude oil outputs amount to about 2mbbl/day. Hopefully these crises can be managed soon.

- OPEC+ actions: OPEC+ is the world largest crude oil export club and it is the single most body that calls the global oil price. At regular club meetings, OPEC+ announces next production targets, it sends strong price signals. But OPEC+ is a club, there is no enforcing mechanism over its members. So, OPEC+ production targets basically are for references. For example, Iraq has indicated that it cannot match the increasing production quota.

Russia seems reached its production limit due to weather and limited investment. This means that, even if OPEC+ is committed to increase crude output, the reality is supply will be tight and global oil price will rise.

- US reality: By and large the Shale Revolution in the US is over now. First of all, Biden administration, like past Democratic administrations, favors green energy over fossil energy. It is a fact that US coal industry was decimated during the Obama administration. By tightening environmental regulations, oil and gas production costs in the US will increase for sure. High crude oil prices contributes to high gasoline price. It inevitably causes inflation and public complaints. But Biden administration has asked OPEC+ to increase output without much success. Biden administration also had asked China, Japan, South Korea, and India for a coordinated release of SPR. Even though, the impact has been largely ignored by the global market.

- We hope the COVID-19 Pandemic is easing now and the next challenge will be the revival of global economy. Energy demand should increase, and the prices will increase too. Balancing economic development with green house emission is also a challenge the world must face.

The following news reports provided the background information.

As if explosions in Nigeria or landslides in Ecuador were not enough, this week has brought another risk factor that was still yet to impact prices – cold. Indeed, a massive winter storm sweeping across the US reached the Permian Basin, triggering fears of potential supply disruptions in the largest American shale play. Add to this the rubber-stamping of OPEC+ production increases into March 2022, completely ignoring the inability or unwillingness of the oil group to stick to its production targets, pepper it with still-ongoing Russia-Ukraine tensions and we have the ideal circumstances for oil prices to surpass the $100 per barrel mark. Oil prices have been on the rise, with Friday’s trading session seeing Brent trading around $93 per barrel, whilst the US benchmark WTI moved to near-parity, trending above $92 per barrel.

OPEC+ Maintains Additions for March ‘22. In a ministerial meeting that lasted a record low of 16 minutes, OPEC+ agreed to extend its 400,000 b/d supply additions into March 2022, brushing aside talks of continuous underperformance of production targets and shrinking spare capacity, strengthening the supertight market sentiment.

Iraq Flags Difficulties Ramping Up Output. Amidst increasing speculation about OPEC+ continuously underperforming its production targets, Iraqi oil company BOC stated that due to limited availability of water for injection, aggravated by the southern fields’ historically elevated water cut, it will not be able to ramp up production tangibly above current levels.

Nigerian FPSO Explodes. A 46-year old floating production and storage vessel exploded off the coast of Nigeria, having some 50,000 barrels in storage at the moment of the blaze – it used to handle light sweet Ukpokiti crude which has not been in production since early 2020.

Cold Spell In Permian Sends Oil Prices Even Higher

By Tom Kool – Feb 04, 2022, 2:00 PM CST

Crude prices rallied on Friday morning as a result of small outages in America’s largest shale play and ongoing political tensions between Russia and Ukraine.

Brent crude touched $90 per barrel briefly this week for the first time in years. This latest jump was attributed to tensions around Ukraine, but this is the most transitory reason for oil price rises. The bigger reasons all have to do with fundamentals. And $90 per barrel of Brent may be only the beginning. A lot has been written recently about OPEC’s spare capacity and the not too rosy outlook for it. That spare capacity is in decline for several reasons, but chief among them appears to be underinvestment. As a result, JP Morgan earlier this month warned that Brent could rise to $125 per barrel as OPEC’s spare production capacity falls to 4 percent of total capacity by the fourth quarter of 2022.

The International Energy Agency has gone even further, warning OPEC spare capacity could fall by half to just 2.6 million bpd in the second half of the year. The agency then went on to say that, “If demand continues to grow strongly or supply disappoints, the low level of stocks and shrinking spare capacity means that oil markets could be in for another volatile year in 2022.”

It is not just OPEC, however. The biggest non-OPEC producer of oil—and biggest oil producer globally—is pumping less than it can. Pressure from shareholders on public oil majors in the United States has increased, as has an insistence that companies focus on greening up their operations instead of looking for more oil and gas to extract. As a result, the U.S. is pumping less oil than it could and, many would argue, should.

As a result, the stage seems set for another expensive year in oil, which happens to coincide with an expensive year overall as central banks begin tightening monetary policies in response to stubborn inflation that, like the IEA’s oil demand forecasts from the early days of the pandemic, proved to be far from the transitory glitch the Fed said it was last year.

“The oil market is heading for simultaneously low inventories, low spare capacity and still low investment,” Morgan Stanley analysts wrote in a note cited by the Wall Street Journal this week, summing up the situation quite nicely. In this situation, $90 for a barrel of Brent may be just the beginning.

Indeed, the Wall Street consensus seems to be that Brent will reach $100 by the summer because of all the reasons listed by Morgan Stanley and also because breakeven costs are also on the rise, thanks to inflation trends and labor shortages, at least in the United States. Yet the biggest driver of prices will remain physical demand.

The International Energy Agency admitted physical oil demand has proven stronger than previously expected in its latest Oil Market Report. Based on this surprising turn of events, the IEA revised up its 2022 oil demand forecast by 200,000 bpd. And based on its track record, it might well turn out it has once again underestimated demand robustness. Even with this estimate, oil demand will not only return to pre-pandemic levels but exceed them, reaching 99.7 million bpd by the end of the year.

In such a situation, higher prices for oil are all but certain since there is precious little—bar another round of lockdowns which is highly unlikely—anyone can do about them. The question, then, becomes how high oil can go before it begins to go down?

The answer is tricky. U.S. public oil companies are still beholden to their shareholders, who seem to be taking to heart forecasts that oil has no long-term future. They have limited space for doing what they want. Private companies will be drilling as WTI continues climbing higher. And OPEC will be drilling as well, but it may choose to keep controls on production rather than switching to “pump at will,” mostly because only a few OPEC members actually have the capacity to pump at will.

Excessively high prices tend to discourage consumption, regardless of the commodity whose prices are getting excessively high. However, there is a caveat, and it is that the commodity must have a viable alternative to discourage consumption when prices rise too high. Judging from Europe’s nightmare autumn and winter this year, alternatives to fossil fuels are not yet up to par. This basically means that the impact of high oil prices on demand will be slow to manifest and slow to push prices down.

Where does this leave the world? The short answer is “Not in a good place.” Higher oil prices will lift the prices of everything else, and this is the last thing you want—if you’re a government—when you’re already struggling with inflation. It may well be that the pandemic will end for good this year, but the real fallout from it may only be starting to show.

By Irina Slav for Oilprice.com